The first enterprises obliged to report on sustainability, as dictated by the CSRD (Corporate Sustainability Reporting Directive) and the ESRS reporting standards, were scheduled to start reporting on their sustainability by the end of this year. These are companies with over 500 employees that work in the public sector.

However, at the end of February 2025, the European Commission presented the legislative bundle Omnibus, which will ease the stipulated regulations and standards and postpone the start of the CSRD Directive, the Corporate Sustainability Due Diligence Directive (CSDDD), and alter the EU taxonomy. The Stop-the-Clock Directive postpones the start of the reporting on sustainability for large enterprises, following the CSRD Directive, by two years. These are companies that would have needed to begin reporting on their sustainability in 2025, as well as SMEs (small and medium-sized enterprises) that trade on the stock market and would need to report on their sustainability in 2026. The other obligations outlined by the CSRD Directive remain obligatory, as does reporting according to ESRS Standards.

Amid the scorching summer, the European Commission surprised us with another set of standards. They unveiled the voluntary VSME standards for SMEs that will introduce a simplified and coordinated reporting system on ESG topics for micro, small and mid-sized companies that need not report under the CSRD Directive. However, as more and more financial institutions and larger companies demand data on sustainability from them, VSME helps SMEs effectively respond to the demands of the supply chain. It facilitates access to financing with more transparent ESG information and helps companies manage their sustainability reporting. In essence, VSME aims to create a more sustainable and inclusive economy. You can learn more about the standard here: VSME Standard.

The most recent piece of information reached us at the end of July, when EFRAG published an amended and simplified version of the European Sustainability Reporting Standards (ESRS). EFRAG now offers a public consultancy service related to the new document, available until 29 September 2025.

Here are the key changes:

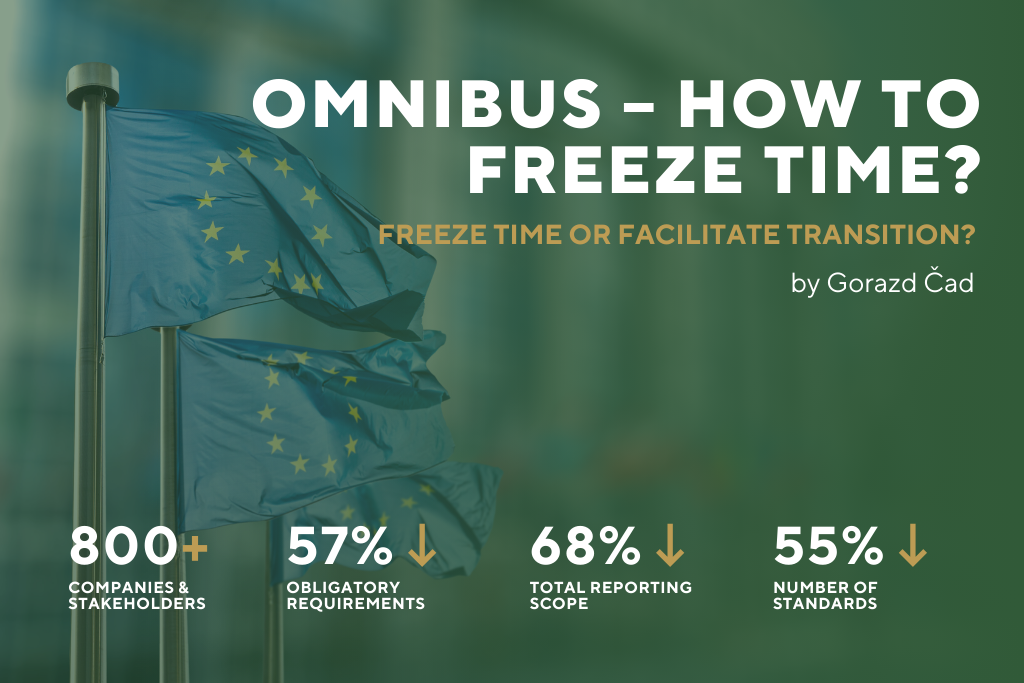

The standards have become simplified and more useful, prepared based on insights and feedback from over 800 companies and stakeholders.

The scope of the reporting will be reduced: the obligatory requirements have been reduced by 57%, and all voluntary requirements disclosures have been removed. In total, the scope of reporting has been reduced by 68%.

The number of standards has been reduced by over 55%, making the process straightforward.

The double materiality assessment has been simplified. The doubling of data will no longer occur, while the language and structure are much clearer.

The new standards also have new exceptions (for instance, exceptions when costs or effort are disproportional).

While the world debates the new simplified sustainability reporting standards, new research by Morgan Stanley has shown that nearly 9 out of 10 companies see sustainability as a prospect for creating value and increasing revenue (higher profits, income growth, less capital expenses). Among over 330 companies, 88% of them state that sustainability directly influences how they strategise. A surprising 53% of them evaluate sustainability as the key engine for producing value, and 35% see it as a combination of creating value and mitigating risk. You can learn more here: https://www.morganstanley.com/press-releases/morgan-stanley-sustainable-signals-survey-2025—morgan-stanley.

We are delighted to hear that many companies still find value in becoming more sustainable. The team at Planet Positive Event will closely follow the latest novelties in sustainability standards (Omnibus, VSME and the revised ESRS), as they represent the foundation for the next version of the tool we will unveil by the end of the year. The new version will be aligned with the ESRS and VSME standards, making our tool the most compatible on the market. That will help us further reinforce the leading status of our tool as a catalyst for facilitating the sustainable transformation within the events industry. The revised standards are a welcome encouragement for event organisers not to freeze their green transition but boost it, with less administration, more alignment with standards and more value for event organisers.

An EU directive establishing mandatory standards on companies’ sustainability impacts, risks, and opportunities, based on the European Sustainability Reporting Standards (ESRS).

ESRS — European Sustainability Reporting Standards

A set of detailed standards setting out how companies report in compliance with the CSRD, covering the full range of environmental, social, and governance (ESG) topics.

VSME — Voluntary SME Reporting Standard

A voluntary standard developed by EFRAG for micro, small, and medium-sized enterprises, enabling simplified disclosure of key ESG information.

SME — Small and medium-sized enterprises

Enterprises with fewer than 250 employees (with specific thresholds for micro, small, and medium-sized categories); in the EU, they account for approximately 99% of all businesses.

EFRAG — EFRAG (formerly: European Financial Reporting Advisory Group)

An EU body that advises the European Commission and develops European positions and standards in the fields of financial and sustainability reporting (e.g., ESRS, VSME).